We love that small businesses are on the rise! That said, not many people start one because they’re passionate about finances.

‘Sorting my finances out’ can be permanent feature on the to do list for many small business owners. People often get stuck because it’s not always clear where to start and, let’s face it, there’s always something more exciting you could be doing.

The lovely people at earnr have shared 5 simple tips for our small businesses community to establish to help get your started:

1. Choose the right set-up

For most, setting up as a sole trader is the way to go. As a sole trader, you’re self-employed and you and your business are one and the same; you’re simply informing HMRC that you’re earning outside of employment. You don’t even need to register straight away. You can earn £1000 a year (the trading allowance) without telling HMRC if you cross that threshold in a given tax year (6th April – 5th April the following year), you have until the following October to register. So if you started after April 6 last year, you have until October 5th this year to register with HMRC if required.

Operating as a limited company (a legal entity registered with Companies House) comes with additional complications and costs relative to being a sole trader. Whilst it might be right for you if you need legal separation from your business or wish to optimise your tax as your profits grow, make sure you understand what’s involved before you jump in.

2. Set up an organised system early

Start keeping a record of your income and expenses from day one. Bookkeeping, as it’s also known, is a critical step in completing a tax return, and it’s much easier to do it as you go than to try and recreate the record later on. earnr makes it simple to capture your transactions by connecting to your bank and importing them daily for you to classify those relating to your business. You can even connect multiple accounts and select the relevant transactions from each.

It’s worth taking the time to capture all your expenses. From a personal perspective, it could result in you paying less tax. Dreamy.

3. Understand your costing and pricing

For any business to be sustainable, you’ll need to understand how much it costs to deliver your product or service and how that relates to the income you generate. Be sure to capture everything you’ve spent money on to inform your pricing decision. Then, consider that cost, the alternatives available, and seek advice on your pricing. Remember, any profits you make as a sole trader should cover the time you put in.

As a rule of thumb, if you get a few paying customers and don’t feel uncomfortable with the price, it could well be too low. We are forever encouraging our customers to value what they produce and charge more!

4. Budget – save for tax and pay yourself

As an employee, your employer takes care of your taxes as you earn. However, that’s different when you operate as a sole trader – HMRC calculates the taxes you owe when you complete a tax return after the end of the year, at which point you might need to make a payment.

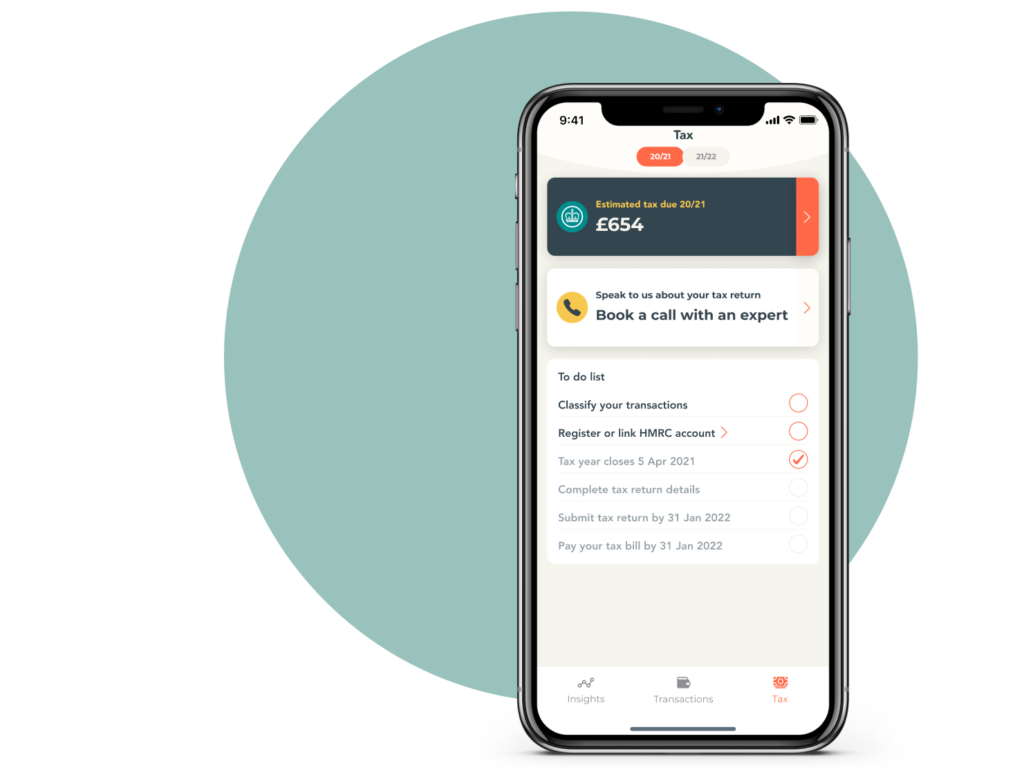

Whilst there are a few ways you can pay, it’s important to save for the bill. Any tax will also be influenced by your other income (e.g. a job). We’ve built a tax calculator into earnr that takes everything into account, giving you an estimated bill that you can save for.

Without the guidance of a tax calculator, we advise you put aside a proportion of your profits – usually 30% or more (to be safe) depending on the tax band of your primary income (see here for more information on tax bands). Using a savings pot linked to your account is a useful way to keep these funds safe. And remember, over saving isn’t an issue, it might well be the case that you’ve saved more than your tax bill, in which case you can put those savings to use elsewhere.

After you’ve saved for your taxes and ensured you have enough funds to continue running the business, you can think about paying yourself. As a sole trader, it’s best to think of this as an allowance. It’s then a case of regularly moving some of the funds generated by the business to your personal funds whilst ensuring your business has enough to operate.

5. Do your tax return early

The tax year closes on April 5th each year. If you’ve recently set up a business, it’s at this point you need to confirm whether you’ve crossed the £1000 allowance and if so, register as a sole trader. For all sole traders, HMRC needs a tax return by the end of the following January. Yes, they give you 10 months to submit it! That said, there are a lot of benefits to doing it early.

First, it’s a review of your business. It’ll help you clarify whether your business is sustainable and, if you set up an organised system, this won’t be a big job.

Second, if your small business is modest relative to your primary income (see self-assessment criteria here), you won’t need to pay a bill. You can pay any tax owed through your tax code instead, and your employer will deduct it over 12 months. Meaning you can put that tax saving pot to good use elsewhere.

Third, if for some reason you’ve overpaid tax, submitting your tax return early is the quickest way to get the refund you’re due.

What next?

At earnr, we’re big advocates of getting organised early. It saves stress, time and money down the line. Plus, with your finances in order, you can get back to building your side income or small business! In line with this, our app is free to use for establishing a record of your income and expenses; take a look here for more info. If you’ve got any questions, feel free to get in contact with Jamie at Jamie@earnr.co.uk, we’re always happy to help!

Leave a comment below with any areas you’d like tips on as a small business owner!